ESTATE PLANNING

| Print this Article |

|

The 3 Tiers of Domestic and International Asset Protection Pools

By Elizabeth Morgan

Everyone needs asset protection to some degree. The greater one’s net worth, the more protection is needed. As early as 1875, the U.S. Supreme Court acknowledged protective structures as a legitimate means of protecting assets from creditors.1 The foundation for this acknowledgment lies in one of the fundamental principles of the unique social experiment that is the U.S. governmental and legal system: To promote a free economy, a free flow of capital is required. And to promote a free flow of capital, citizens must feel free to create capital without undue fear of reprisal, debtors prison, or destitution, all consequences that could befall an entrepreneur in the countries from which the founders of the U.S. came. As a result, this unique system was designed to promote and encourage the creation of capital and to discourage undue financial risk by creating safeguards against undue risk.

However, as the U.S. legal and judicial system has developed, some of the safeguards instituted by the founding fathers have increased the potential for creditors’ claims. The current American legal system encourages litigation because it is not a loser-pay system, unlike other Western systems. Instead, it allows contingency fees and punitive damages against individuals, and it does not require bonds to file suit except in the case of an appeal.

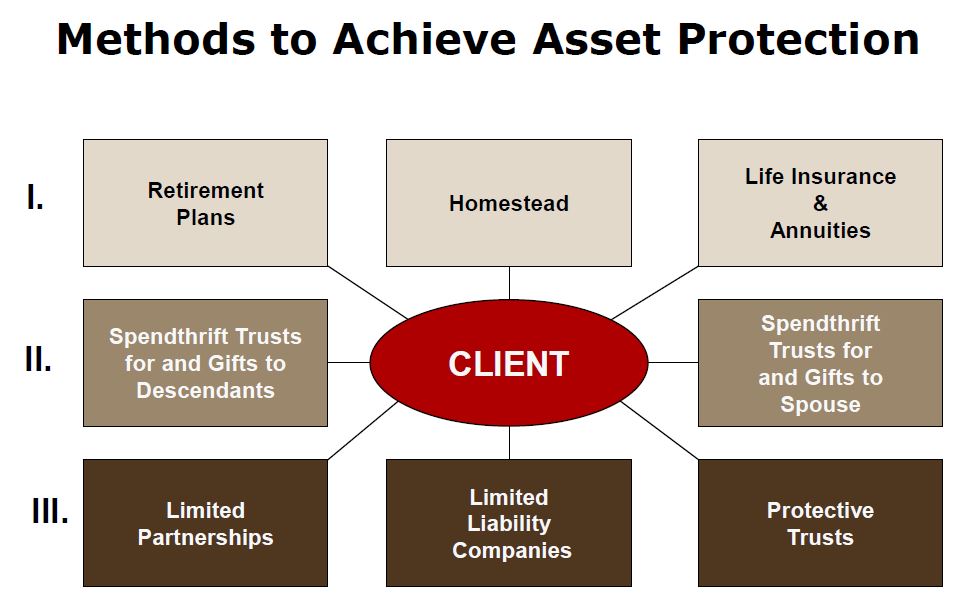

Protecting assets from the claims of future creditors should be done in a thoughtful and proactive manner that neither disadvantages current creditors nor leaves assets vulnerable to future, unknown creditors. Because it is impossible to predict from where the threat will arise or what the future will hold, it is advisable to fill as many protected buckets as possible. One way to think about a protective structure is to think of it as buckets divided into three tiers and to fill each bucket with as much as possible, starting with the first tier and proceeding to the second and third tiers as necessary. Understanding these tiers will help you to assess whether your clients are adequately protected and whether they could consult a lawyer to explore more sophisticated techniques.

Tier One: Statutorily Protected Asset Classes

The first tier consists of statutorily created protected classes of assets: retirement plans and education savings plans; homestead; and life insurance and annuities. Not every state statute is the same, but the general rules are consistent, and filling these buckets up to the statutorily protected limits is a great first step in creating a wealth protection plan. The cash value of ERISA-qualified retirement plans is generally fully protected. Internal Revenue Code Section 529 accounts and other education savings plans are also generally protected up to a certain value.

Next, depending on the state, all or a portion of the value of an individual’s homestead will be protected from creditors. Some states exempt up to a certain value of equity in a home, while other states (like Texas and Florida) protect a certain amount of acreage without regard to value. The cash value of life insurance and annuities is also protected from the claims of creditors in most states (others, like California, protect only up to a certain amount of cash value). Remember, though, only the cash value and the death benefit are protected. If the cash is either distributed out of a life insurance policy or an annuity, then the cash in the hands of a debtor will be available to satisfy the claims of creditors.

Tier Two: Trusts

The second tier of protected buckets consists of trusts for descendants and spouses. Other types of protected trusts, like charitable and split-interest trusts, provide some protection as well. These irrevocable trusts are based upon a specific trust structure that does not allow the beneficiaries to make voluntary or involuntary transfers of trust funds, thereby causing the assets to be protected from the claims of the beneficiary’s creditors.

Important here is the utility of a well-drafted premarital agreement. Pre- and post-marital agreements can create clearly defined property parameters, thereby lessening exposure to each other upon divorce. They can also protect the children and other interested parties upon the death of one of the partners in the relationship. Furthermore, a properly drafted agreement can segregate property of the underexposed spouse so that creditors cannot reach him or her.

Tier Three: Protected Entity Structures

If, after filling the buckets in the first and second tiers, a client still has unprotected and vulnerable assets, it will be necessary to use the buckets in the third tier.

Entity structures such as limited partnerships and limited liability companies put a wall between the assets of the owner of the company and the assets of the company itself. The company is a distinct legal entity, separate from its partners. In a limited partnership, the general partner manages the entity and is liable for partnership liabilities. The remaining partners are liable only up to the amount of their contribution to the partnership. In a limited liability company, management of the company is handled by an outside manager or members. Members are liable for company liabilities only to the extent of their contribution to the company.

Companies can be useful protective structures because many states have passed legislation codifying charging orders as the exclusive remedy against such structures. A charging order is an order issued by a court that charges the debtor’s interest in the entity with the amount due to the judgment creditor. Under a charging order, the creditor only gets distributions from the entity to the extent of the debt. Once the debt is extinguished, the charging order is fulfilled. The debtor’s interest in the underlying partnership or company assets is preserved.

When considering limited partnerships and limited liability companies as avenues for asset protection, it is important to ensure the entities are established in jurisdictions that provide statutory protection for interests in these types of entities. Be sure to transfer control of the entity away from any creditor-exposed owner and to segregate entity assets into separate, siloed entities. It is also important to ensure that the owners of any protective company structure comply with the necessary reporting laws, such as the Corporate Transparency Act, which established new reporting requirements for owners of corporations, limited liability companies, and other registered entities who exercise “substantial control” over the company or own 25% or more of the company.

Tier Three: Protective Trusts

There are two types of protective trust structures: domestic and foreign.

Domestic protective trusts are available in 19 states, with the most recent legislative adoption of the structure coming from Connecticut in 2020. Domestic protective trusts are useful, but the U.S. court system retains jurisdiction over the trust and, therefore, its assets. Furthermore, domestic protective trusts can be subject to punitive damages and costs of attorney fees.

Offshore protective trusts offer additional benefits. Creditors cannot reach foreign trust assets through the U.S. court system. In fact, U.S. judgments against foreign assets are not enforceable. Legal actions, to be enforceable, must be pursued offshore, and the cost of pursuing the foreign assets is high. Many offshore jurisdictions are loser-pay-all jurisdictions, so creditors may find the cost of the fight to be too high.

Dynastic trusts can be domestic or foreign. They include the benefits of a basic wealth protection trust, including the retention of the settlor’s beneficial interest and the settlor’s ability to make a completed gift. Dynastic trusts may avoid gift, estate, and generation-skipping transfer tax. It is important to establish these trusts in a jurisdiction that is friendly to perpetual trusts.

These Tiers Can Help Build Asset Protection

All of us need asset protection to some degree, and using this convenient three-tier matrix as a pattern for compiling a protective structure can be a useful first step in building that structure.

1. See Nichols v. Eaton, 91 U.S. 716, 725-726 (1875) (Justice Samuel Freeman Miller).

Elizabeth Morgan, founder of Elizabeth Morgan & Associates LLC, represents clients with multijurisdictional tax, estate, and business planning issues. She is the author of the four-volume Domestic and International Law and Tactics, the foremost treatise on asset protection.

image credit: istock.com/ilkercelik