RETIREMENT PLANNING

| Print this Article |

|

Third Grade Math and Retirement Contributions

By By James L. Evans, CFP®, QPA, QKA, ChSNC

Over the last few years, I have observed a trend in industry articles that imply saving for retirement via a Roth type contribution is almost always more beneficial than the traditional retirement savings option. Although I understand the many concepts and arguments in favor of this type of approach, I thought it might be beneficial to do the math.

Fuzzy Math

I like math, I like details, and I like bothering people with math and details. The practice of math leads—you hope—to solutions. But mathematical solutions often create controversy. We have all heard the Benjamin Disraeli quote made famous by Mark Twain: “There are lies, damn lies, and then there are statistics.” More recently, the term “fuzzy math” was used by President George W. Bush in a debate with Al Gore. Then-candidate Bush was critiquing parts of Gore’s economic plan. The funny thing is there is a branch of mathematics known as Fuzzy Math or Fuzzy Set Theory; it is a method of applying the precision of math to an ambiguous or uncertain set of variables. So—let’s get fuzzy!

In the third grade or thereabouts we all learned about the communicative, associative, and distributive properties. For those who do not remember the third grade, these properties essentially say the order does not matter—the same facts lead to the same solution. (Apologies to all third grade math teachers for the oversimplification!)

Let’s apply those principles to determine which type of retirement contribution to choose: traditional or Roth.

A Hypothetical Example

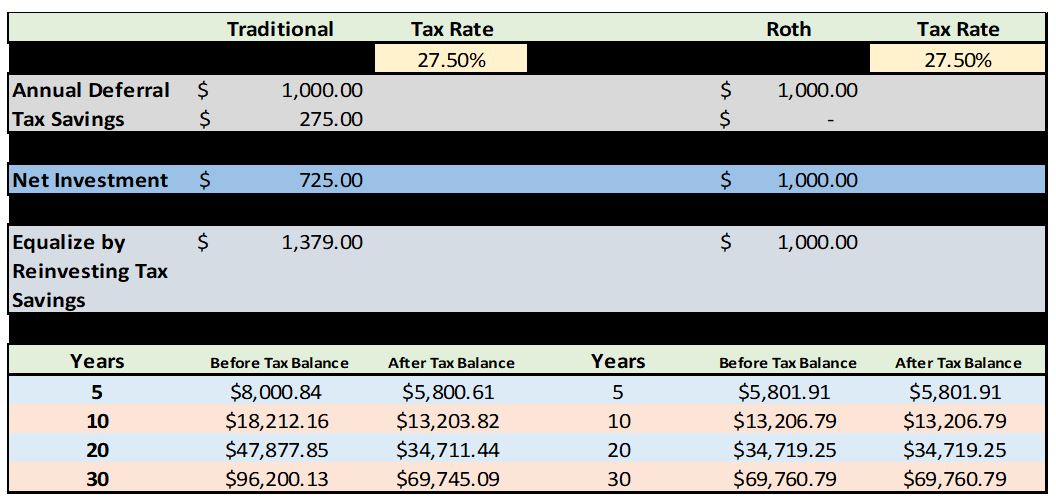

Let’s say you’re working with a married couple earning over $207,000 after the standard deduction—so we will assume their marginal bracket is 24%. Say they live in Ohio—one of the 43 states that have income tax as well—so that adds another 3.5%. Thus, our couple has a marginal tax rate of 27.5%.

Presented with the opportunity to contribute to either a traditional or Roth IRA as part of their retirement plan, which would work out better? What are the important variables?

The table below compares a traditional versus Roth contribution for our couple—assuming a $1,000 contribution.

On the Roth side of the grid, a $1,000 deposit requires a $1,000 reduction in pay. On the traditional side, to deposit a net of $1,000 out of their pay, the couple would have to deposit $1,379 into the plan: $1,379 x .725 = $1,000.

The second portion of the grid shows the $1,000 accumulating at 5% over various time periods. The after-tax balance under the traditional side assumes the couple can pull their money out at the same marginal rate they were under while working.

Assuming their tax rate remains the same and they equalize the equation by investing their tax savings, the after-tax result is exactly the same for the traditional and Roth. However, there are two important variables.

One is mechanical. Does the couple have the will and discipline to equalize the equation by investing their tax savings? Does the couple need a Roth to act as a sort of forced savings vehicle for them?

The second is something beyond their control. Will their tax rate increase or decrease by the time they start drawing on their account balance—to the degree their marginal rate decreases in retirement the traditional IRA will be more beneficial and vice versa?

The first question is subjective based on each personality. But how does a planner answer the second question about something as fuzzy as marginal tax rates?

Do we plan on the couple earning more in retirement than while working? Do we assume the federal and/or state government will increase the marginal rates over time?

Roth Versus Traditional in Retrospect

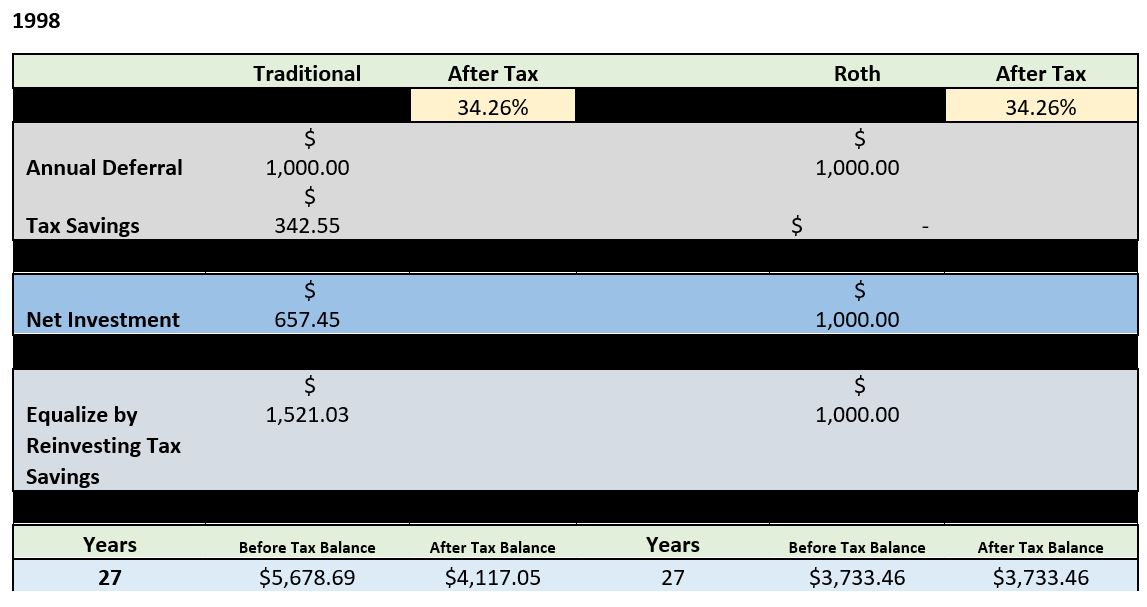

We can answer the question in retrospect. Let’s take the same couple, rolling back their income for inflation (using the Minnesota Fed’s Inflation Calculator) to 1998 and applying the federal and state tax marginal rate at that time:

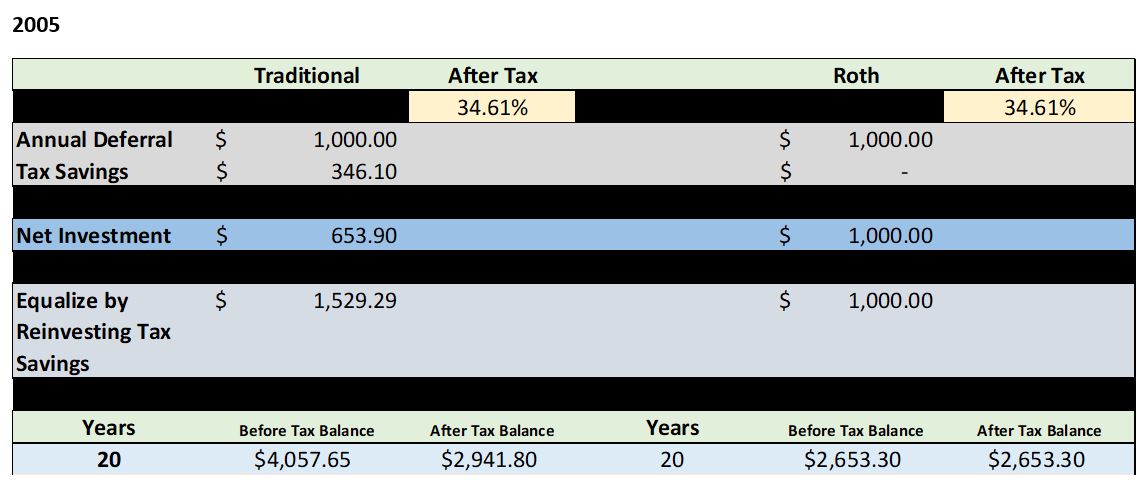

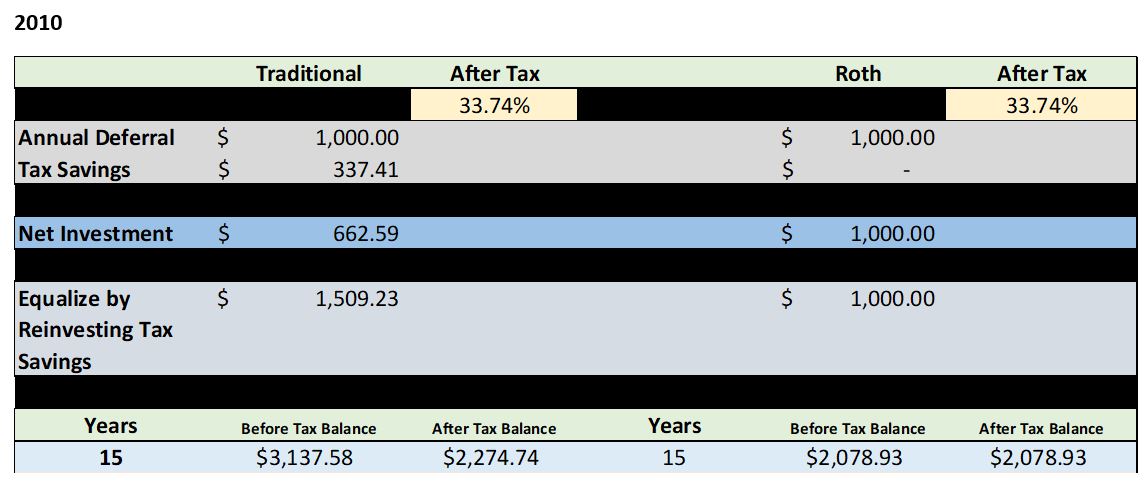

In this particular case and for this particular year, it was better to make the contribution before-tax by quite a bit. Admittedly, the result could vary year to year. So, let’s look at 2005 and 2010.

In each case with these particular facts, this client was better off saving via the traditional retirement before-tax method. It is just math.

Could things change? Could marginal rates increase dramatically? Could their income increase dramatically? Sure. But all things being equal since the Roth rolled out, it has not happened that way.

One could argue this extended period of relatively modest income tax rates will inevitably be followed by a period of high rates. Again, that could happen. But there are a lot of ways to raise money: tariffs and the Affordable Care Act are two recent examples.

What is the point of all this math?

Given the inherent uncertainty of future tax laws and economic conditions, why is the advice so consistently “Roth everything”? In this case, and one would suspect many other cases, it would have been more beneficial to take the deduction—at least thus far.

Where Do We Go From Here?

Developing a methodology that informs our recommendation of traditional versus Roth contributions would help. We tailor investment allocations based on risk appetite, age, and account purpose to maintain an efficient investment allocation for clients. We do this even though we do not know what future investment results will be. The unknown future is exactly the reason to create an efficient portfolio. Why not develop a framework for Roth versus traditional decisions? This framework might include the current tax bracket and career trajectory—the goal being to optimize a client’s tax efficiency in retirement even when faced with unpredictable future conditions.

Here’s another way to say it: If all of a client’s savings were Roth at retirement, that would be very inefficient. The client would almost certainly have paid taxes at a higher rate during their working years than they would be paying on their first dollars drawn each year in retirement.

If we agree 0% is an inefficient tax rate then what is an efficient tax rate in retirement? What combination of before- and after-tax savings would be most efficient?

The answer requires a multivariable equation. I’ll let you do the fuzzy math.

Epilogue

Despite my love for math, I recognize numbers don't tell the whole story. As Einstein said, “Not everything that counts can be counted, and not everything that can be counted counts.” For some folks, not having a hanging tax liability will give them more comfort than selecting the optimal math solution. For instance, paying off a mortgage early, even with a low interest rate, provides a sense of security that's hard to quantify. That just might be better for some than executing the best mathematical solution. For these folks, a Roth IRA brings them comfort and peace of mind. And that you cannot count.

Jim Evans has been in the financial services business for 39 years. In October 2006, he co-founded TTG Financial. Jim and his wife Jill live in Northeast Ohio. They have two children and three grandchildren.

image credit: Adobe Stock Images