Wholesale Prices Move Up In May

![]() Print this Article | Send to Colleague

Print this Article | Send to Colleague

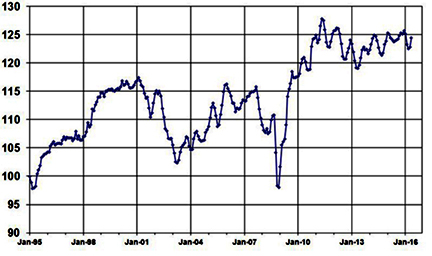

Wholesale used vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) increased in May, resulting in a Manheim Index reading of 124.5. The large monthly rise, combined with weakness this time last year, resulted in a year-over-year gain – the first since December of last year. The Manheim Used Vehicle Value Index stood at 124.5 for May.

Consecutive increases in the Manheim Index in April and May do not suggest a reversal in the expected downward trend in pricing as a result of higher wholesale supplies. They do suggest, however, that dealers have continued to achieve efficiency gains that are allowing them to bid up auction prices even as gross margins narrow. That’s encouraging to commercial consignors who have been expecting, and preparing for, greater weakness in wholesale pricing.

"Are financial markets pointing to credit contraction?" That was the question we posed in our February Index release given the gyrations in the global markets at the time. Those issues have yet to be resolved.

According to Fed Funds futures, May’s weak employment report greatly reduced the odds of a Fed rate hike this month. But that was never the issue. We are more interested in market reactions to Fed moves than in the moves themselves. Consider, for example, that even a well-telegraphed, small quarter-point rise and a dovish press conference in December caused harmful reverberations throughout January and early-February.

Interpreting reactions to what will likely be inaction by the Fed will be harder, so we are left with comments and discussions with industry participants. They are not encouraging. Being the cleanest shirt in the closet no longer impresses investors. Groupthink is taking hold, and that thinking is not positive.

Rental risk prices ease further. Auction prices for rental risk units, adjusted for market class shifts and mileage, declined again in May; but the year-over-year decline was substantially less than in either April or March. A straight average of rental risk units sold at auction had an increase in pricing for both the month and year-over-year. The difference between the two series was driven primarily by the reduction in average mileage, which, in May, fell to its lowest level since September 2014.

New vehicle sales: So-so again. New car and light-duty trucks sold at a seasonally adjusted annual selling rate (SAAR) of 17.4 million in May, slightly better than April’s 17.3 million pace, but below last May’s 17.6 million rate. Given differences in trading days, number of weekends, where holidays fall, and promotional activity, it is best to look at the SAAR on a three-month moving average basis. By that measure, it was 17.1 million in May.

For the first five months of 2016, the SAAR averaged a modest 17.2 million – and that was despite heavier fleet sales. In the first five months, new vehicle purchases increased 8 percent for rental car companies, 11 percent for commercial fleets, and 38 percent for government agencies.

At the start of the year, there were indications that manufacturers were going to accept the leveling-off of sales at last year’s record pace; but announced incentives for June picked up. Overall, new vehicle inventory levels are reasonable; but the mix is imbalanced. On net, we expect the new vehicle market will have a slightly negative impact on used vehicle residuals in the coming months.

Used vehicle sales continue to show steady increases. According to NADA, total used retail unit volumes increased 4 percent in the first five months of 2016, with franchised dealers up 3 percent, independents up 6 percent, and private party transactions up 4 percent. Likewise, CPO sales, were also up 4 percent in the first five months of 2016, and thus are on track for their sixth consecutive year of record sales.

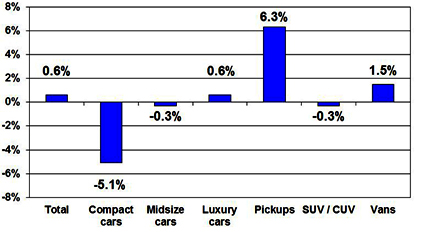

Did compact car prices find a floor? In May, the mileage and seasonally adjusted measure of compact car prices jumped up more than 2 percent. If you’re optimistic, view it as a "dead cat bounce." Year-over-year, compact cars remained the weakest segment – and they too had a sizable number of off-lease units coming back. So, yes, if a floor was found, that would be a good thing.

Unadjusted prices remain high. Due to the share shift toward commercial consignment and lower average mileage for both dealer and commercial consignment, a straight average of auction prices remained well above year-ago levels in May.

Consecutive increases in the Manheim Index in April and May do not suggest a reversal in the expected downward trend in pricing as a result of higher wholesale supplies. They do suggest, however, that dealers have continued to achieve efficiency gains that are allowing them to bid up auction prices even as gross margins narrow. That’s encouraging to commercial consignors who have been expecting, and preparing for, greater weakness in wholesale pricing.

"Are financial markets pointing to credit contraction?" That was the question we posed in our February Index release given the gyrations in the global markets at the time. Those issues have yet to be resolved.

According to Fed Funds futures, May’s weak employment report greatly reduced the odds of a Fed rate hike this month. But that was never the issue. We are more interested in market reactions to Fed moves than in the moves themselves. Consider, for example, that even a well-telegraphed, small quarter-point rise and a dovish press conference in December caused harmful reverberations throughout January and early-February.

Interpreting reactions to what will likely be inaction by the Fed will be harder, so we are left with comments and discussions with industry participants. They are not encouraging. Being the cleanest shirt in the closet no longer impresses investors. Groupthink is taking hold, and that thinking is not positive.

Rental risk prices ease further. Auction prices for rental risk units, adjusted for market class shifts and mileage, declined again in May; but the year-over-year decline was substantially less than in either April or March. A straight average of rental risk units sold at auction had an increase in pricing for both the month and year-over-year. The difference between the two series was driven primarily by the reduction in average mileage, which, in May, fell to its lowest level since September 2014.

New vehicle sales: So-so again. New car and light-duty trucks sold at a seasonally adjusted annual selling rate (SAAR) of 17.4 million in May, slightly better than April’s 17.3 million pace, but below last May’s 17.6 million rate. Given differences in trading days, number of weekends, where holidays fall, and promotional activity, it is best to look at the SAAR on a three-month moving average basis. By that measure, it was 17.1 million in May.

For the first five months of 2016, the SAAR averaged a modest 17.2 million – and that was despite heavier fleet sales. In the first five months, new vehicle purchases increased 8 percent for rental car companies, 11 percent for commercial fleets, and 38 percent for government agencies.

At the start of the year, there were indications that manufacturers were going to accept the leveling-off of sales at last year’s record pace; but announced incentives for June picked up. Overall, new vehicle inventory levels are reasonable; but the mix is imbalanced. On net, we expect the new vehicle market will have a slightly negative impact on used vehicle residuals in the coming months.

Used vehicle sales continue to show steady increases. According to NADA, total used retail unit volumes increased 4 percent in the first five months of 2016, with franchised dealers up 3 percent, independents up 6 percent, and private party transactions up 4 percent. Likewise, CPO sales, were also up 4 percent in the first five months of 2016, and thus are on track for their sixth consecutive year of record sales.

Did compact car prices find a floor? In May, the mileage and seasonally adjusted measure of compact car prices jumped up more than 2 percent. If you’re optimistic, view it as a "dead cat bounce." Year-over-year, compact cars remained the weakest segment – and they too had a sizable number of off-lease units coming back. So, yes, if a floor was found, that would be a good thing.

Unadjusted prices remain high. Due to the share shift toward commercial consignment and lower average mileage for both dealer and commercial consignment, a straight average of auction prices remained well above year-ago levels in May.

Tom Webb is chief economist for Cox Automotive. Contact him at Tom.Webb@coxautoinc.com or follow him on Twitter at @TomWebb_Manheim.

Tom Webb is chief economist for Cox Automotive. Contact him at Tom.Webb@coxautoinc.com or follow him on Twitter at @TomWebb_Manheim.

![]()

![]()

![]()

![]()