Mission Not Impossible: Growth in Mature Markets

Print this article | Send to Colleague Print this article | Send to Colleague

Pulp & paper industry focus and value creation logic have been largely based on production efficiency instead of top line revenue growth. However, the main driver for investment decisions in the future will be more focused on the search for new markets and growth, according to a recent article in Pöyry's Executive Wire titled "Mission Not Impossible: Growth in Mature Markets."

Times of structural change often bring out market dictated needs for strategy change and force companies to direct attention to new opportunities, the article notes. When the demand development ticker starts to stay horizontal or move south, it means increasing competition for the remaining tons in the market. This basic premise is accentuated by the paper industry's high fixed cost structure and high exit/entry barriers which often lead to pushing tons into the already saturated market place. Feeble demand coupled with over capacity sets the stage for weak pricing—where supply side market power has not been established. Value is about to get destroyed--unless...

Note: The following is excerpted directly from the Pöyry article. For more information or further discussion, contact Soile Kilpi, principal, soile.kilpi@poyry.com (646-651-1547), or Sanna Kallioranta, consultant, sanna.kallioranta@poyry.com (225-281-1366).

Growth avenues for pulp and paper companies

Growth in mature and declining markets is possible but requires well-thought-out strategy and actions. The following growth strategies (market dominance, market segmentation, new markets, new businesses) describe four different but valid approaches to unlock top line value creation. However, none of these strategies works all of the time. Every situation is unique and careful consideration should be given to the development of your individual strategy. Sometimes it pays to walk to the beat of a different drummer. Growth in mature and declining markets is possible but requires well-thought-out strategy and actions. The following growth strategies (market dominance, market segmentation, new markets, new businesses) describe four different but valid approaches to unlock top line value creation. However, none of these strategies works all of the time. Every situation is unique and careful consideration should be given to the development of your individual strategy. Sometimes it pays to walk to the beat of a different drummer.

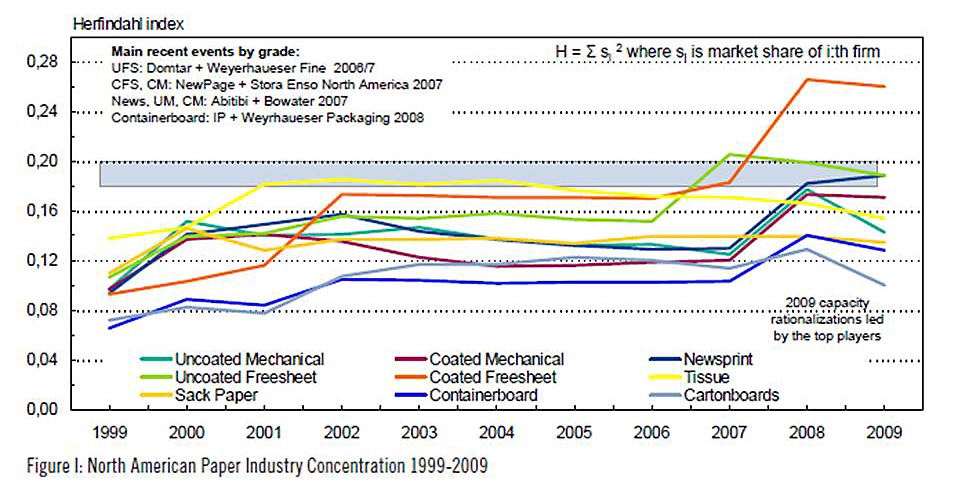

1. Market Dominance: From survival of the fittest to thriving of the biggest. Many sectors of the paper industry have already undergone a couple of "warm up" rounds of consolidation. The future rounds are about becoming the dominant player. We have seen pre-plays of that unfolding in several segments. In the uncoated free sheet (UFS) market, Domtar's acquisition of Weyerhaeuser's assets in 2007 doubled Domtar's capacity and placed the company on the top of the North American UFS market with 35% capacity share. In the current industry structure, only International Paper is in the same size league with Domtar, with 26% capacity share.

The coated free sheet (CFS) market in North America has the highest consolidation level in the paper industry. NewPage, Sappi, and Verso are the sector captains with a combined 84% market capacity share, although, their dominance has been seriously pressed by the influx of Asian coated paper imports. Before the recent tariffs imposed on coated paper imports, the U.S. International Trade Commission estimated that the Chinese and Indonesian producers held more than a quarter of the market.

Market dominance might sound like a straight-forward strategy but it is far from it, both in strategic planning and operational execution. One of the fundamentals is the decision to become the dominant player in the right market category and geography. Although AbitibiBowater is the dominant player with 35% newsprint capacity share in North America, it was unable to avoid Chapter 11, filing in April 2009. The second largest newsprint producer, White Birch (18% capacity share), followed suit in February 2010.

2. Market Segmentation: Not all rivers are created equal. A lot of market side attention should be given to identifying or creating pockets of sustainable demand opportunity. These pockets of opportunity may be found within the existing product grade markets through customer segmentation that targets specific end-uses, market needs, or buyer behaviors. Alternatively, these opportunities might be found from alternate product grade markets. We have seen moves by commodity players gradually gearing up in specialty segments:

-

Verso's Bucksport mill has shifted its focus from coated mechanical to specialty packaging and uncoated grades and developing niche products

-

Boise Inc., although maintaining the top four position in uncoated free sheet, has placed more emphasis on packaging and specialty label and release markets

-

Several dissolving pulp manufacturers have geared their business model towards pulp making by-products, chemicals, as well as manufacturing more value added pulp grades, such as acetate pulp, high tenacity filaments, ethers, lyocell, special textile filaments, and nitro-cellulose, etc.

Also bolder moves have taken place. International Paper has been changing its printing and writing paper focus history to a packaging focused future. In 2005, 52% of IP's asset base was in printing and writing grades. By 2010, that share has dropped to 29%.

3. New Markets: The developing world is your oyster. When markets at home have started to decline, but you possess strong capabilities in a market category, it is time to examine entry into new geographic markets to unlock value creation. Globalization was a hit theme in the paper industry in the 1990s. Especially European paper companies made big moves entering North America (Stora Enso acquired Consolidated Papers, UPM-Kymmene acquired Blandin and Miramichi mills) and emerging markets (UPM-Kymmene joined forces with APRIL, Norske Skog acquired mills in Thailand and Korea).

Again, expansion to new geographies sounds like a straightforward strategy, but is anything but. Since the globalization boom, many of the grandiose moves have been scaled back for various reasons ranging from challenges in partnership selection to underestimating the complexity of entry and business integration involved. North American players were more prone to stay at home (could there be a correlation with 75% of Americans not having a passport?).

Half of the 10 largest North American paper companies have production assets only in the domestic market. International Paper and Georgia-Pacific have been by far the most active companies in building if not world dominance, at least worldwide presence. International Paper has mills in eight countries, including Brazil, China, Mexico, and several European countries. Georgia-Pacific has mills in 11, mainly European, countries.

4: New Businesses: New seas, new fish. The pulp & paper industry, as an expert of fiber flows, inherently possesses many opportunities to enter new business areas, beyond paper. Some traditional paper industry companies have started corporate repositioning in new sectors. For example, UPM-Kymmene is building its future on strategy that integrates bio, energy, and forest industries into a newly coined term—"biofore" industry. Cascades is building up its waste management footprint through its subsidiary recycling operations—Metro Waste. In 2009 Cascades announced the acquisition of the Canadian assets of Sonoco Recycling and the recovery assets of Yorkshire Paper Corp., both which provide collection services for recyclable materials including corrugated containers, paper, and plastics.

Some companies have chosen to acquire new positions within the paper value chain. Glatfelter's acquisition of Concert in early 2010 instantly positioned it as a leading global supplier of absorbent cellulose-based, airlaid non-woven materials, which are used in many consumer and industrial applications with growing global demand, including feminine hygiene, adult incontinence products, and specialty wipes. Also in early 2010, Mohawk Fine Papers announced the acquisition of LabPrints, which offers workflow integration solutions for professional photographers and photo labs. The LabPrints acquisition strengthens and widens Mohawk's position in the digital printing value chain.

2010 might become an interesting year of transactions and strategic moves.

|

|